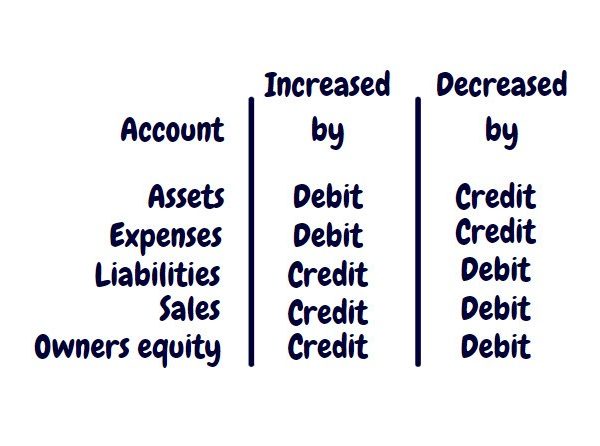

I still remember my first accounting class as a 15-year-old. My teacher, Mr Gledhill, a speedo wearing surfer dude teacher marked up the formula below on the whiteboard.

This is the accounting equation.

Gledhill then tried to convince us that bookkeeping followed one of Newton’s laws of physics which says for every action there is an equal and opposite reaction. Well in bookkeeping, for every transaction there is an equal and opposite transaction. This is the law of double-entry bookkeeping.

For every debit, there is an equal and opposite credit.

Mr Gledhill then wrote on the table below, illustrating how debits and credits work in relation to the accounting equation.

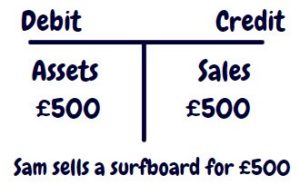

Sam’s Surf Shop was his local hangout at the weekend, and always his favourite reference.

Sam sold a surfboard for £500 cash, how would this transaction be accounted for? Well, we’re increasing cash. Cash is an asset. So we debit assets by £500, increasing them.

Sam has also made a sale so we want to increase sales by £500. So we credit sales £500.

Gledhill took to the whiteboard to illustrate one of his famous T equations. Debits on the left and credits on the right.

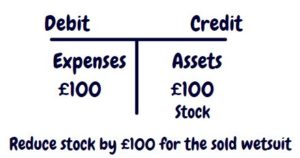

Next, he said, Sam uses the £500 cash he’s just received to purchase some wetsuits. How would the T equation look here?

We’ve purchased stock (i.e. wetsuits), stock is an asset. So we debit stock.

We’ve paid with cash, so we’ve decreased an asset. To decrease an asset we need to credit it.

Gledhill took to the whiteboard once more.

That’s it Gledhill said, you now understand the accounting equation and double-entry bookkeeping. A simple little process that’s a pillar of modern-day capitalism.

Bonus question:

Gledhill took to the board one last time, if Sam paid £500 for 5 wetsuits and he sold one of the wetsuits for £250.

1. How much margin did he make?

2. What are the T accounts for this transaction?

And, he made a margin of £150. Margin = sales – expenses.

James Watson