You’ve set up a Limited Company – about to start the empire – what next? How will it all work for tax, what else do you need to think about…?

These are familiar questions and it can all seem a bit daunting at the start. If you’ve ditched the Corporate world to set up as a freelancer, you were no doubt used to a monthly pay cheque and not having to worry about tax (except getting annoyed about how much was deducted each month). If you’ve managed to bypass the trappings of IR35 and set up as a Limited Company then good news. Hopefully you’re going to save some tax, but there are a few things you’ll need to think about…

How do you pay yourself? If your Limited Company is going to be profitable then you will want to pay yourself with a mixture of salary and dividends. This is usually the most tax efficient way to do things.

How does that actually work? You need to register your Limited Company for PAYE with HMRC. Once you’re registered, the Company can run a payroll. You can then add yourself onto the payroll, and run yourself a monthly payroll going forwards. You have to report this to HMRC monthly. Accounting software like Xero or Quick Books will let you run payroll and link up to HMRC for all the reporting they need.

What salary do you pay yourself? You want to pay yourself just below the National Insurance threshold. This is the maximum salary you can pay yourself before you have to pay any tax. For tax year 22/23 this is £758.33 per month, or £9,100 per year. That’s probably not quite going to be enough for the bills I can hear you saying, this is where the dividends come into play…

Dividends? A Company can declare dividends from its profits once it has paid any Corporation tax due. For example, in your first year your Limited company makes a net profit before tax of £35,000 – that’s any income less any business expenses and running costs. The Company will need to pay Corporation tax, which will be more or less calculated at 19% on the profit before tax.

So, £35,000 x 19% = £6,650 of corporation tax to pay over to HMRC.

That leaves £35,000 – £6,650 = £28,350 profit after tax. That is available to declare as a dividend to the shareholders. A dividend is the shareholders taking the profit out of the Company. Important to note that dividends must always be ‘declared’ in line with the shareholdings. If you are the only shareholder then it’s simple. But if there are two 50/50 shareholders, the dividends will always need to be declared 50/50 to those shareholders.

You don’t have to declare the dividend. You can leave that profit in the Company if you don’t need it personally. It rolls forward in your Company ‘Retained Earnings’ and you can declare a dividend in future years. You’ll have more cash in your business bank A/C.

How are dividends taxed? You have to report dividends declared in your annual personal self-assessment tax return, and that’s where you pay tax on them.

How much then? Here’s the good bit, dividend tax rates are lower than income tax rates. Everyone also gets an annual dividend tax free allowance of £2,000 (tax year 22/23). This is on top of your tax-free personal allowance of £12,570 (tax year 22/23). Dividends are taxed as follows:

- Basic rate – 8.75% (compare to 20% income tax)

- Higher rate – 33.75% (compare to 40% income tax)

- Additional rate – 39.35% (compare to 50% income tax)

Quick recap on taxes please? Ok so here’s what you’ll need to remember:

- Corporation tax – Paid by your company on its net profit, currently fixed at 19% (tax year 22/23). You pay this annually after your Company year end. You have to submit a CT600 to HMRC (Corporation tax return), and you get 12months after the end of your year end to submit the return. Note – you have to pay any tax due 9 months after year end, so it’s best to get it submitted within the 9months.

- PAYE/ National Insurance – If you are able to declare dividends from your Company, as outlined above we, recommend paying yourself a salary of £9,100 per annum which would mean to PAYE or NI to pay. So, nothing to worry about here.

- Dividends – You need to report the dividends you have declared from your Company in your personal self-assessment, and that’s where you pay the tax on those. You have to file your self-assessment (and pay any tax) by 31 January following the end of the tax year (so nearly 10months after). Note – if your tax bill is over £1k, you may need to start paying in advance. HMRC call this ‘payments on account’ – explained here.

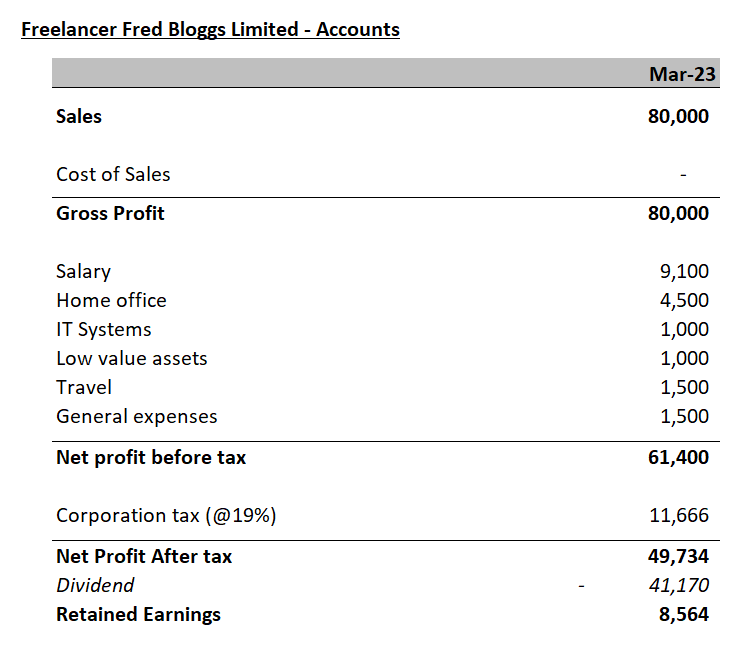

This all makes sense, but what’s the optimum set up? Good question – and it depends on how much you’re earning. Let’s say you will have £80k of income into your Limited Company in your first year. Your profit and loss might look something like this:

The Company is profitable so you can pay yourself the £9,100 salary and keep below the National Insurance threshold. You have £11,666 of Corporation tax which you will need to pay from the Company. You would have until the start of January 2024 to pay this after your March 2023 year end.

You then have £49,734 available to take as a dividend.

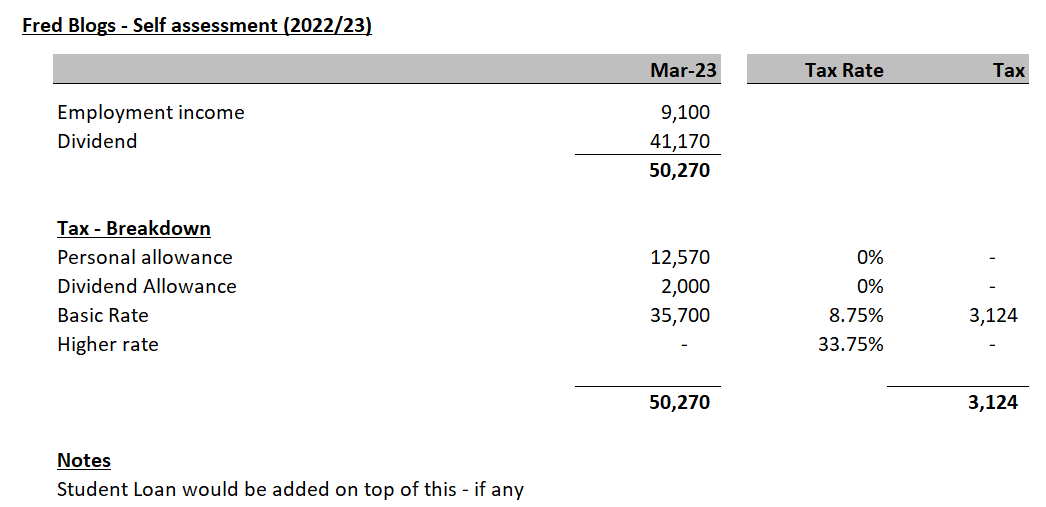

Onto the self assessment: If we then look at Fred’s self-assessment. We’re assuming Fred has no other sources of income from property, investments etc (100% focused on growing the new empire!) He will need to report his salary of £9,100 from the Company, and any dividends he has declared.

On the dividends, the tax rate up to the basic rate is low at 8.75%, so it’s sensible to declare dividends up to that basic rate. In Fred’s case he can declare a dividend of up to £41,170, and he would have £3,124 of tax to pay in his self-assessment.

Any additional dividend Fred declares will be taxed at 33.75% so it gets more expensive. If he can afford to keep the remaining £8,564 of profit in the Company to roll forward it’s probably sensible.

What else do I need to think about? It’s difficult but it’s really important to know if you are going to be profitable before you go down the salary + dividends route. If you try and declare dividends from your Company but you don’t have the profit, you end up in an overdrawn Director’s loan position. This is bad, and there are tax consequences.

Student loan – Another important point – if you’re paying your student loan off, this will get calculated and repaid based on salary + dividends in your self assessment.

Timing is key – You pay tax on dividends based on when they are declared, you need a dividend voucher to support dividends reported in your self-assessment. You just need to think about the timing of which tax year you’re reporting your dividends. Fred’s Limited Company year-end is March. That’s straight forward because it’s in line with the personal tax year (5th April – 6th April).

To conclude – If this is all still completely over your head, this is a very bread and butter set up for PennyBooks. We help lots of freelancers and small Limited Company business owners achieve an optimum set up like this, so get in touch!

James Watson